District 5 Condos - A 10 Year Study

March 22, 2025

Statistics and Trends

March 22, 2025

Statistics and Trends

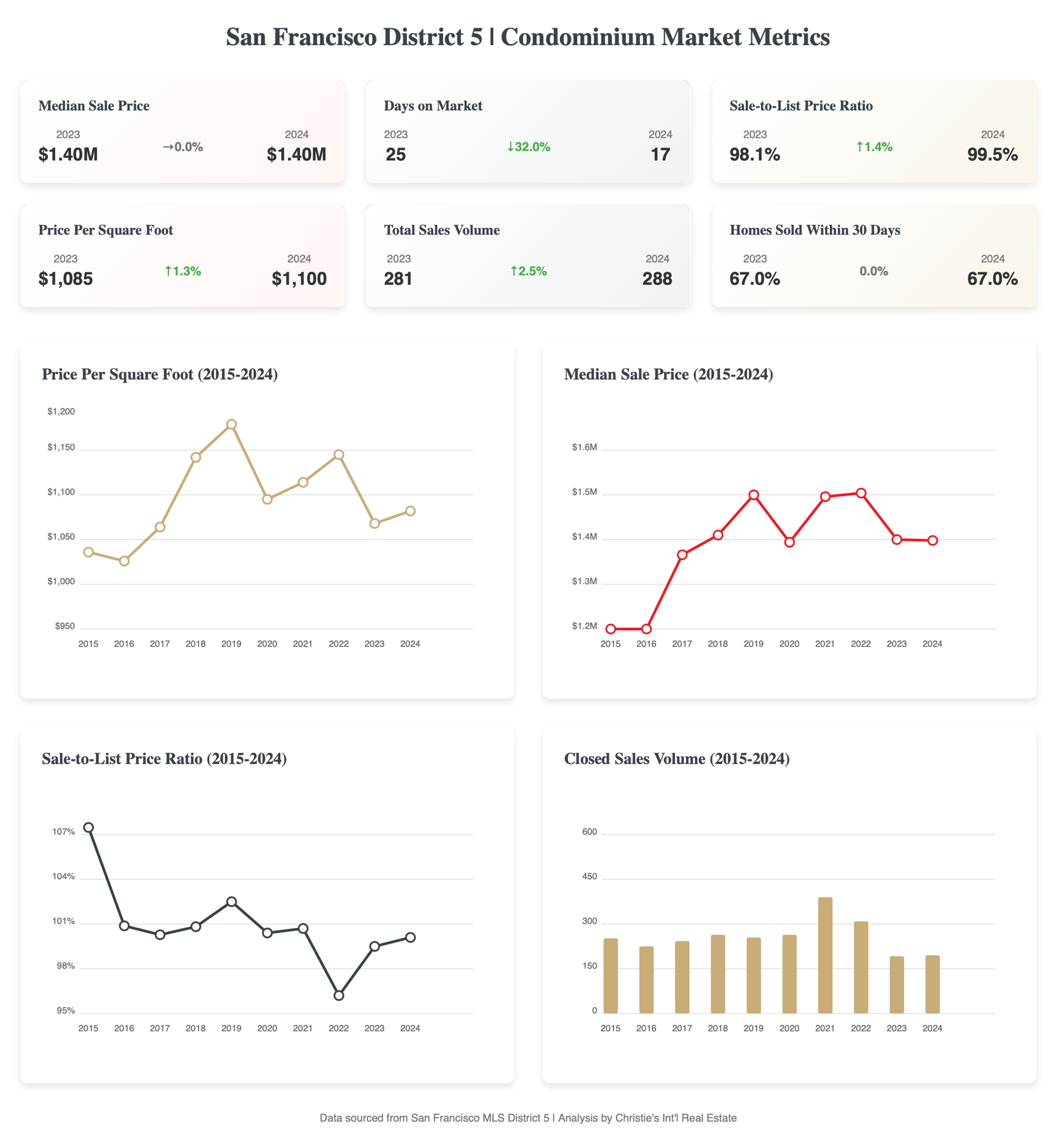

After years of unprecedented pandemic-driven volatility, San Francisco's District 5 condominium market is showing clear signs of stabilization in early 2025. Our analysis of a decade of transaction data reveals a market that has weathered significant disruption and is now finding its footing in a more sustainable pattern. This detailed examination offers insights into both obvious and subtle shifts across Mission Dolores, Duboce Triangle, Castro, Noe Valley, Haight Ashbury, Glen Park, and other coveted District 5 neighborhoods.

While the raw data shows sales volume grew modestly from 281 units in 2023 to 288 units in 2024 (a 2.5% increase), this seemingly minor uptick represents a critical inflection point. The market appears to have definitively bottomed out after plummeting from the pandemic-driven surge of 575 transactions in 2021.

What's particularly telling—and easily overlooked—is the composition of these transactions. The percentage of properties selling within 30 days increased from 58% in 2023 to 67% in 2024. This 9-point jump suggests inventory is moving more efficiently despite persistent interest rate challenges, indicating stronger buyer conviction than overall volume would suggest. So far, 2025 is continuing that trend (although not part of the analysis as we don't yet have a full year of data).

The median closed price of $1.4M remained virtually unchanged between 2023 and 2024, following a modest correction from the $1.5M peak in 2022. This price plateau, now extending into early 2025, shouldn't be misinterpreted as market weakness. Rather, it represents:

What's less obvious in the headline numbers is the growing disparity between premium and standard properties. Properties with desirable attributes (outdoor space, home offices, updated systems) are commanding increasingly significant premiums over baseline comparable properties.

Perhaps the most revealing insight from our analysis is the stark contrast in sale-to-list price ratios based on days on market:

This 11.5 percentage point spread reveals we're effectively operating in two distinct markets simultaneously:

This bifurcation is easily masked by the overall average ratio of 99.52% but represents crucial intelligence for both buyers and sellers developing their 2025 strategies.

As we look ahead, several strategic implications emerge for sellers:

The San Francisco District 5 condominium market has completed its post-pandemic adjustment phase and is now demonstrating clear stabilization patterns. The measured improvement in key metrics suggests a sustainable recovery taking shape in 2025. We're seeing early signs of gradual volume growth following the 2023 bottom, with transaction numbers beginning to climb steadily. Price stability has returned after the correction from 2022 peaks, creating a foundation for potential modest appreciation as buyer confidence returns. Market efficiency continues to improve, as evidenced by the compression in average days on market from 25 days in 2023 to 17 days in 2024. Additionally, the significant premium commanded by properties selling quickly (107.98% of list price for homes selling within 30 days) highlights the continued and growing advantage for turnkey, well-prepared homes.

This analysis is provided by The Binnings Team of Christie's International Real Estate, based on MLS data for San Francisco District 5 from 2015-2024, with preliminary observations from Q1 2025.

Stay up to date on the latest trends

June 23, 2026

Your insider guide to what’s happening on both sides of the bridge!

June 15, 2026

Eight new spots to watch on both sides of the bridge.

June 8, 2026

Wine Country, Coastal Retreats, and Mountain Getaways

June 2, 2026

A thoughtful approach to updating homes in the Bay Area.

News

May 27, 2026

A breakdown of why some SF homes spark bidding wars while others linger on the market.

May 26, 2026

Your insider guide to what’s happening on both sides of the bridge!

News

May 6, 2026

When considering amenities for the bath and laundry spaces, new homeowners have specific wish-list items and designs.

April 27, 2026

Your insider guide to what’s happening on both sides of the bridge!

April 21, 2026

Illuminate Your Home with Style, Intention, and Local Flair

From strategy to sold

The Binnings Team is one of the Bay Area's most successful agent teams, consistently ranked among the top-performing agents in San Francisco and Marin. Whether you're buying or selling a home, we can help you get the most for your investment.